How Everyday Decisions Quietly Turn Into Financial Traps

Most people don’t fail financially because of something dramatic.

It’s not the big mistake.

Not the bad investment.

Not even the wrong career choice.

It’s something quieter.

It’s the belief that they’re fine… when they’re not.

The Illusion of “I’m Okay”

I’ve seen this play out more times than I can count.

Someone in their 40s or 50s has:

- a house

- a job

- a retirement account

- maybe $50,000… maybe $100,000 saved

And they feel… okay.

Not rich.

But responsible.

They’ve done what they were supposed to do.

Then something shifts.

A job loss.

A market drop.

A health issue.

And suddenly, the system is exposed.

Two People, Same Life… Different Outcome

Two people.

Same salary.

Same neighborhood.

Same career length.

Let’s call them Robert and Daniel.

Robert

Robert has about $80,000 saved.

He feels good about it.

When someone suggests he should save more, he says:

“I’ll get serious next year when things settle down.”

Daniel

Daniel has about $90,000 saved.

But he did something Robert didn’t.

He sat down one night… and did the math.

He realized:

That money wouldn’t support him.

Not even close.

So he made a decision that didn’t feel good.

He cut expenses.

He increased his savings.

He started immediately.

Ten Years Later

Robert: ~$160,000

Daniel: ~$310,000

The difference wasn’t income.

It was how they interpreted reality.

Safety Is Not a Feeling

This is one of the most dangerous traps people fall into:

Feeling safe instead of being safe.

Your brain rewards progress with relief.

“I’ve saved something.”

“I’ve made it this far.”

“I’m doing better than most.”

But your brain runs on emotion.

Your system runs on math.

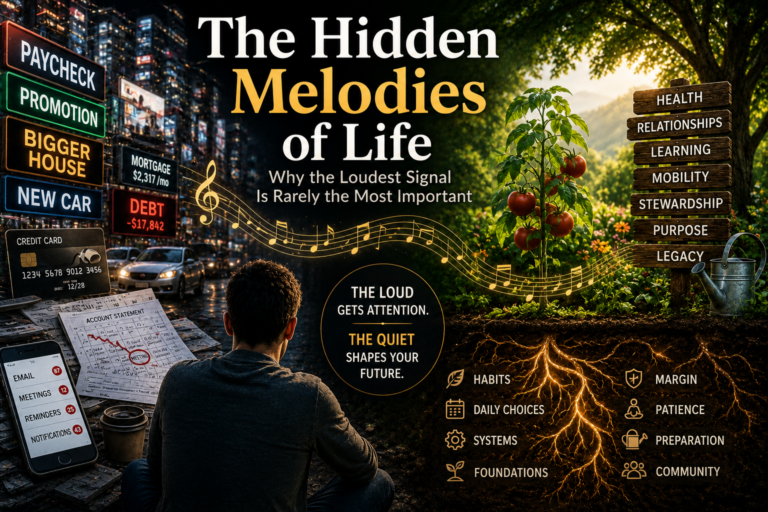

The Real Problem Isn’t Income

Here’s where it gets uncomfortable.

Most people could improve their situation.

But they don’t.

Not because they can’t…

Because their life is locked in place.

The Lifestyle Cement

By your 50s, your spending isn’t just spending.

It’s identity.

- the house

- the car

- the vacations

- the way your family lives

- what your friends expect

These aren’t just expenses anymore.

They’re load-bearing walls.

Try removing one and you don’t just save money…

You feel like you’re going backwards.

I’ve seen people:

- keep a $700 car payment

- maintain a lifestyle they can’t support

…while quietly losing their future.

Not because they’re irresponsible.

Because they’re human.

The Real Risk Nobody Talks About

Let’s go one layer deeper.

You could do everything “right”…

And still lose.

Two retirees.

Same savings.

Same withdrawal.

One retires into a strong market.

The system grows.

The other retires into a downturn.

They withdraw while the system is shrinking.

They never recover.

Same discipline.

Same plan.

Different timing.

This is called sequence risk.

But you don’t need the term to understand the impact.

The 2-Year Moat (This Changes Everything)

Most advice says:

“Have 3–6 months saved.”

That’s fine for survival.

But it’s not enough for strategy.

A 2-year reserve does something completely different.

It gives you time.

And time changes everything.

Imagine This

You lose your job.

Scenario 1 — No Buffer

You:

- panic

- take the first job

- accept lower pay

- lose negotiating power

Scenario 2 — 2-Year Moat

You:

- evaluate options

- wait for the right opportunity

- retrain if needed

- negotiate from strength

Same person.

Different system.

Different life.

This Isn’t About Money

That reserve is not just dollars.

It is:

- time stored

- pressure reduced

- options preserved

It protects you from:

- selling at the wrong time

- accepting the wrong deal

- making decisions under pressure

It protects your decision quality.

The Garden Version

If you’ve ever grown anything, you’ve seen this.

A garden without water storage must react immediately.

Plants suffer while you scramble.

A garden with reserves responds calmly.

Adjusts.

Stays alive.

Same garden.

Different system.

The Part Nobody Prepares For

Now let’s go deeper.

I’ve seen people retire “successfully”…

…and fall apart within a year.

Not financially.

Mentally.

Physically.

Because they lost:

- structure

- purpose

- something to build

At first, it feels like freedom.

Then it feels like drift.

A financial plan without a life plan is incomplete.

The Real Shift

Most people think wealth is:

how much you have.

But it’s not.

It’s:

- how your system behaves under pressure

- how long you can wait

- how well you can choose

A Simple Exercise (Do This Tonight)

Write down:

- Your total savings

- Multiply by 0.07

- Divide by 12

That’s your monthly income from savings.

Now write your monthly expenses.

The difference?

That’s your gap.

Not your balance.

Not your feeling.

Your gap.

Where This Connects

If this feels uncomfortable, that’s a good sign.

It means you’re starting to see the system clearly.

If you want to strengthen the foundation behind these numbers:

→ Read: Soil Before Stocks

If you’re wondering how to actually start improving your system without overwhelm:

→ Read: The 1% Garden Rule

Closing

You don’t need a perfect system.

You need a real one.

Because in the end:

The people who do well are not the ones who felt safe.

They are the ones who built systems that actually were.

This is just one piece of a much larger system.

The more pieces you connect, the clearer the picture becomes.